When I came across the details of the Wazir-e-Azam Apna Ghar Program, my first thought was — this is exactly the kind of initiative millions of Pakistani families have been waiting for. If you have been paying rent every month while watching your savings sit idle, this scheme deserves your full attention. The government, through the State Bank of Pakistan, has structured a housing finance program that genuinely addresses the affordability barrier that has kept homeownership out of reach for most middle-income Pakistanis.

I want to be direct with our readers at Pak Public Portal: this is not just another announcement that sounds good on paper. The numbers here are real, the participating banks are operational, and the markup rate of 5% fixed for the first 10 years is one of the lowest offered on any formal housing finance product in Pakistan’s recent history. Whether you live in Karachi, Lahore, Peshawar, or a smaller city — if you have a valid CNIC and you are a first-time homebuyer, this scheme was built for you.

Let me walk you through everything — eligibility, loan details, property size limits, how to apply, and answers to the questions most people are asking right now.

About the Wazir-e-Azam Apna Ghar Program

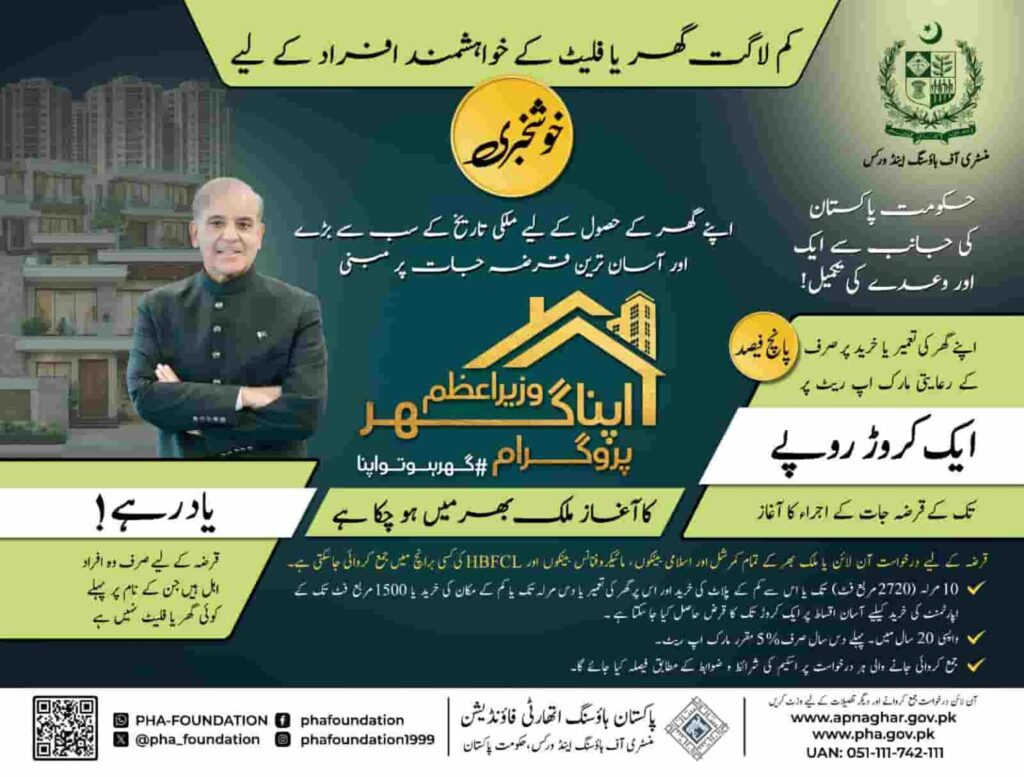

Wazir-e-Azam Apna Ghar Program This program is an affordable housing finance program introduced by the federal government and governed through the State Bank of Pakistan (SBP). The main objective of this program is to increase ownership of houses among Pakistani citizens who have never had homes before. To do this, the program has provided the participants with subsidized markup rates and flexible repayment periods as well as to reduce the large housing gap existing in Pakistan for the last several decades.

The strengths of this program include the use of more than one banking channel. This allows participants of the program not to go to the same bank but rather provides an option for them to receive loans from a bank close to their home. This is made possible due to the participation of commercial banks, Islamic banks, microfinance banks, and the House Building Finance Company Limited (HBFCL).

Another strength of this program is the Shariah compliance feature. This can be achieved by using Islamic banking channels, which are free from any sort of conventional interest. This strength demonstrates the seriousness behind introducing this government program.

Scheme at a Glance — Key Features Table

| Feature | Details |

|---|---|

| Maximum Loan Amount | PKR 10,000,000 (1 Crore / 10 Million) |

| Minimum Equity (Applicant’s Share) | 10% of property value (LTV: 90:10) |

| Loan Tenure | Up to 20 years (maximum) |

| Markup Rate – First 10 Years | Fixed 5% per annum |

| Markup Rate – After 10 Years | 1-Year KIBOR + 3% (variable) |

| Maximum House Size | 10 Marla / 2,720 sq. ft. |

| Maximum Apartment/Flat Size | 1,500 sq. ft. |

| Property Value Cap | No upper cap |

| Processing Fee | None |

| Prepayment Penalty | None |

| Administering Authority | State Bank of Pakistan (SBP) |

Scheme Type: Government Housing Finance Program

Coverage: All of Pakistan

Participating Institutions: All Commercial Banks, Islamic Banks, Microfinance Banks, HBFCL

Last Date to Apply: June 30, 2026

Allowed Uses for Loans

This is an important segment, since not all expenditures related to housing can be considered. There are three allowed uses under this Wazir-e-Azam Apna Ghar Program:

- Purchase of a new or existing house/apartment which fulfills the requirements of minimum size

- Construction of a house on an owned plot if you do not have enough money for construction

- Purchase of a plot together with construction of a house on this plot

The uses which are explicitly disallowed include reconstruction or repair of an existing house. If you want to renovate an existing house, then this scheme does not help you. Also, purchasing of a plot without any plans for its construction does not fit into the above criteria.

Eligibility Criteria

Nationality & Documentation

- Must be a Pakistani citizen with a valid CNIC

- No dual nationality restrictions mentioned in the scheme guidelines

First-Time Homeownership

- The Wazir-e-Azam Apna Ghar Program is exclusively for first-time homebuyers — applicants who do not currently own any residential property anywhere in Pakistan

- You will be required to submit a sworn affidavit (halaf-nama/undertaking) confirming you have never owned a home before

- If this declaration is later found to be false, the subsidy must be returned and a financial penalty will be imposed

Income & Co-Applicants

- There is no fixed minimum or maximum income requirement stated at the scheme level

- You may combine your income with a co-applicant (such as a spouse or family member) to increase loan eligibility

- Final credit assessment is done by the bank based on their internal policies

Age

- No specific age limit has been set by the scheme itself

- Individual banks may apply their own credit and age-related criteria during assessment

How to Apply — Step by Step

- Identify your nearest participating bank — any commercial bank, Islamic bank, microfinance bank, or HBFCL branch across Pakistan

- Visit the branch in person and ask specifically for the “Apna Ghar Scheme” / Wazir-e-Azam Housing Finance application form

- Collect the required documents list from the bank representative — typically includes CNIC, proof of income, property documents, and the affidavit form

- Prepare your affidavit confirming first-time homeownership — this can usually be done through a notary or oath commissioner

- Submit your completed application with all supporting documents to the bank branch

- Bank conducts credit assessment — they will evaluate your income, CNIC records, and property details

- Upon approval, the bank processes the loan disbursement as per the agreed schedule

- Repayment begins as per the agreed tenure (up to 20 years)

There is no online central application portal mentioned — the process is branch-based through participating banks.

Important Terms and Conditions

- The maximum loan amount under this scheme is PKR 10 million — no exceptions

- Applicant must contribute a minimum of 10% of the property’s total value from their own funds

- For the first 10 years, the markup rate is fixed at 5% per annum — it will not change regardless of market fluctuations

- From year 11 onwards, the rate becomes variable at 1-Year KIBOR + 3%, which will be adjusted annually

- No processing fee is charged under this scheme : Wazir-e-Azam Apna Ghar Program

- No prepayment penalty — you can pay off the loan early without any additional charges

- Property size must not exceed 10 Marla (2,720 sq. ft.) for houses or 1,500 sq. ft. for apartments

- A false affidavit results in subsidy recovery plus financial penalty

- Bank employees can also apply if they are not eligible for their employer bank’s internal housing finance

- The scheme covers all property types that meet size criteria — no restriction on property value ceiling

Reasons to Consider this Scheme

Wazir-e-Azam Apna Ghar Program Indeed, there is little use in elaborating on the problem this project seeks to resolve since everyone who pays rent in Pakistan’s cities is painfully aware of their troubles. For the past several years, the cost of renting property in cities such as Karachi, Lahore, and Islamabad has risen to the point that people typically continue paying rent for the rest of their lives without ever owning anything.

One of the main features of the project that caught my attention is the guaranteed 5% interest for the first decade. This is not a sales pitch trick but rather a real rate fixed by the government through SBP. When compared to other commercial mortgages with interest rates ranging from 18-22%, it becomes evident why the scheme could be appealing.

Moreover, the fact that there is no processing fee and no penalty for early repayment of the debt makes one feel free to do whatever suits them best. In case their finances improve after five years, for instance, they are able to get rid of the loan without worrying about being penalized for it.

For young professionals, married couples saving up for their first home, or families currently living on rent — I genuinely recommend visiting your nearest bank branch and having an initial conversation with their loan officer. Even if you are not 100% sure about eligibility, getting a preliminary assessment costs nothing.

Contact Information

If you need help with a Wazir-e-Azam Apna Ghar Program scheme you can get guidance and assistance from these people:

- State Bank of Pakistan is a place to start you can visit their website at www.sbp.org.pk.

- House Building Finance Company Limited is another option their website is www.hbfcl.com.pk.

- You can also go to any branch of a bank in Pakistan, like Allied Bank or Habib Bank Limited or MCB Bank or UBL or Meezan Bank or Bank Al-Habib.

- If you prefer Islamic Banks you can try Meezan Bank or Bank Islam or Dubai Islamic Bank.

- For Microfinance Banks you can look at Khushhali Bank or NRSP Microfinance Bank.

- Official Website: www.apnaghar.gov.pk

- UAN (Helpline): 051-111-742-111

Frequently Asked Questions (FAQ)

- Is there an age limit to apply for the Wazir-e-Azam Apna Ghar Program?

The program does not have an age limit. This is news for young people and those in their 40s and 50s. Each bank will assess your credit. Consider your age and loan period. For example a 55-year-old applying for a 20-year loan may be viewed differently than a 30-year-old. You should visit your bank and ask. They will give you an answer.

- Who can apply for this housing scheme?

Any Pakistani citizen with a CNIC who is buying or building a home for the first time can apply. You do not need to be a government employee or have an income. The scheme is open to salaried people, self-employed people and business owners. Long as the bank is satisfied with your creditworthiness.

- How will the bank verify that I am a first-time homeowner?

You will need to submit a signed affidavit that you do not currently own any property in Pakistan. This is a document. If it later turns out that you already owned a property and submitted a declaration you will have to return the entire subsidy amount and pay a penalty.

- Can a husband and wife apply together. Combine their incomes?

Yes you can. This is a feature of the scheme. If your individual income does not qualify for the loan amount you need you can add a co- usually a spouse. And combine both incomes to improve eligibility. Banks have the discretion to accept income clubbing so discuss this option during your bank visit.

- What is the maximum loan amount available under this Wazir-e-Azam Apna Ghar Program scheme?

The maximum financing available is PKR 10 million. This is the ceiling. No bank can offer more than this amount under the Apna Ghar scheme. However you can always make a larger down payment if the property costs more than what the loan covers.

- How much of my money do I need to bring?

You need to contribute at least 10% of the total property value as equity. So if the property is worth PKR 5 million you need to arrange at PKR 500,000 from your own pocket. The bank finances the remaining 90%.

- What is the Wazir-e-Azam Apna Ghar Program markup rate for the 10 years ?

For the first 10 years of your loan the markup rate is fixed at 5% per annum. This rate will not change no matter what happens to market interest rates. You get predictability in your monthly installment for 10 full years.

- What happens to the rate Wazir-e-Azam Apna Ghar Program after 10 years?

From year 11 onwards the rate shifts to a structure. Specifically 1-Year KIBOR plus 3%. KIBOR changes over time based on market conditions so your installment will be adjusted annually after the 10-year fixed period ends.

- Are there any fees or early payment charges?

No. The scheme explicitly states no processing fee and no prepayment penalty. If you want to pay off the loan five years early you are free to do so without any financial penalty.

- How long can I take to repay the loan?

The maximum repayment tenure is 20 years. You can choose a period if you prefer. Some people opt for 10 or 15 years to reduce total interest paid.

- What size of property can I. Build under this Wazir-e-Azam Apna Ghar Program?

For houses the allowed size is 10 Marla. For apartments or flats the maximum is 1,500 feet. There is no cap on property price.

- Can I use this loan to renovate my existing home?

No. This scheme is strictly for purchasing a home buying an apartment constructing on an owned plot or buying a plot and constructing simultaneously. Renovation or repair of an existing property is not covered.

- Which banks are offering this scheme?

All major commercial banks in Pakistan are participating, along with banks, microfinance banks and HBFCL. This includes banks, like HBL, UBL, MCB, Allied Bank, Bank Alfalah, Meezan Bank, Bank Islami and others. Just walk into any branch. Ask specifically for the Wazir-e-Azam Apna Ghar Program application.

Disclaimer

The information published on Pak Public Portal regarding the Wazir-e-Azam Apna Ghar Program 2026 has been compiled from official scheme details and publicly available sources for the benefit of our readers. Pak Public Portal is an independent information platform and is not affiliated with the State Bank of Pakistan, any participating bank, or the Prime Minister’s Office. Readers are advised to verify all details directly with their respective bank branches or HBFCL before making any financial decision. Loan approval, eligibility, and terms are subject to the policies of the individual participating financial institutions. Pak Public Portal bears no responsibility for any discrepancy between information published here and actual scheme terms at the time of application.

More Details pakpublicportal.com